The access inflection: Wegovy moves toward PBS, generics upend global pricing, and 7.8 million Australians are now formally eligible

The first quarter of 2026 marks a structural turning point for the Australian GLP-1 market. Health Minister Butler committed to listing Wegovy on the PBS in January — the first subsidised obesity weight-management medicine in Australia's history — while price negotiations with Novo Nordisk remain unresolved and a listing date of late 2026 or early 2027 appears likely. Simultaneously, the March 20 expiry of semaglutide's core patent in India triggered a Day 1 launch by over 15 generic manufacturers, crashing prices 90% and setting a long-lead pricing signal that will ultimately reach Australian shores when domestic patent protections expire in the 2030s. Eli Lilly's April refusal to list Mounjaro on the PBS despite a positive PBAC recommendation signals a deepening pricing standoff between global pharma and the Australian government that will shape the GLP-1 access landscape for years ahead.

PBS access imminent — but contested

Wegovy is heading to PBS under narrow criteria (BMI ≥35 + CVD), while Lilly's Mounjaro just withdrew its PBS application due to pricing stalemate. Two GLP-1s, two very different government relationships.

India's patent cliff is live

15+ Indian manufacturers launched generic semaglutide on March 20. Australia's own patent protection runs to the 2030s — but the global pricing floor is being set now, and it will inform PBAC negotiations.

Chemist Warehouse is the GLP-1 channel

Sigma Healthcare's results confirm GLP-1 dispensing is now a structural growth driver. With oral forms expected in Australia by late 2026, CW's dispensing advantage will only compound.

Three imminent decision points: (1) Wegovy PBS listing date and final price — negotiations with Novo Nordisk are the critical bottleneck; (2) whether Lilly re-submits Mounjaro to PBAC under a new pricing structure; (3) TGA timeline for oral semaglutide and orforglipron registration, expected late 2026.

| Domain | Activity Level | Top Signal | Australian Impact |

|---|---|---|---|

| Regulatory & Access | ● High | Wegovy PBS commitment; Mounjaro PBS withdrawal | Direct — listing imminent |

| Compounding & Supply | ● High | TGA April peptide warning; Ozempic Supply Only | Direct — enforcement active |

| Generic & Patent | ● High | India patent expiry March 20; 15+ generics launched | Global-pathway — AU patent until ~2030s |

| Clinical Pipeline | ● High | Oral semaglutide US launch; orforglipron FDA approved; 7.8M AU eligible | Adjacent — TGA filings underway |

| Pharmacy & Retail | ● High | Chemist Warehouse +17.2% GLP-1 sales; Priceline M&A | Direct — channel reshaping now |

| Consumer & Supplements | ● Medium | Food reformulation emerging; protein supplement demand rising | Emerging — early-stage in AU vs US |

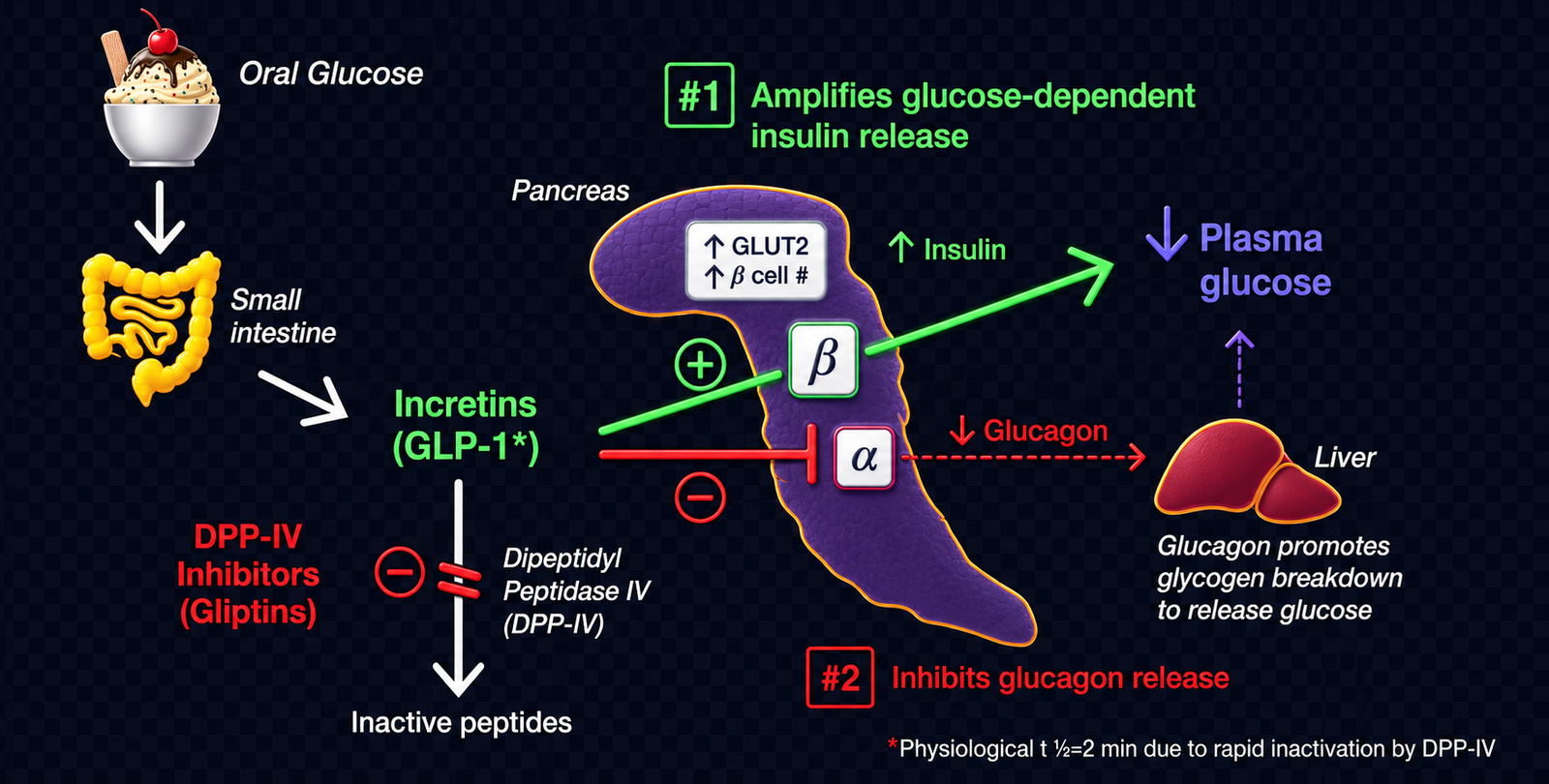

A plain-English explainer for readers who want the mechanism behind the market shift.

PBS, TGA, PBAC decisions, scheduling changes, and reimbursement pathway developments.

Health Minister Mark Butler publicly committed to listing Wegovy (semaglutide 2.4mg, Novo Nordisk) on the PBS following the PBAC's November 2025 recommendation. The listing would apply to adults with established cardiovascular disease (prior MI, stroke, or symptomatic peripheral arterial disease) and BMI ≥35 kg/m² (≥32.5 for Asian, Aboriginal, or Torres Strait Islander populations). More than 400,000 Australians are currently paying up to $5,000/year privately for GLP-1 medicines. Minister Butler acknowledged a "very big bill for taxpayers" while framing the decision as an equity issue. PBS Medicine Status website confirmed notice of intent lodged February 20, 2026; price negotiations with Novo Nordisk had not yet commenced as of February 28, 2026. (Sources: ABC News 12 Jan 2026; PBS Medicine Status website; SBS News 12 Jan 2026)

Eli Lilly has refused to list Mounjaro (tirzepatide) on the PBS for type 2 diabetes, despite a positive PBAC recommendation following the drug's fourth PBAC submission (March 2026). Lilly stated the Australian government was unwilling to pay a "fair price," while the Australian Financial Review reported the stand-off is part of a broader pricing dispute between the US and Australia over PBS pricing. This is the fourth consecutive failure for tirzepatide at PBAC (previous submissions: July 2023, November 2024, and a re-entry attempt). Mounjaro currently costs $285–645/month on private prescription in Australia. (Sources: AFR 24 Apr 2026; Medical Republic 25 Apr 2026; MedNews 6 Mar 2026)

Eli Lilly's Mounjaro (tirzepatide) was resubmitted to the PBAC in early March 2026, marking the drug's fourth attempt at PBS listing — this time for type 2 diabetes. PBAC has previously declined to recommend tirzepatide at its July 2023 and November 2024 meetings. The April withdrawal confirmed the fourth attempt also failed to result in a listing. (Source: MedNews 6 Mar 2026)

PBS Schedule data confirms Ozempic (semaglutide 1.34 mg/mL, both 1.5 mL and 3 mL pen devices) is listed as "Supply Only until 01/06/2026." Under Supply Only status, products remain available for dispensing — pharmacies can fill existing prescriptions — but new prescribing against the PBS item code is restricted. This is a meaningful supply-side constraint: GPs cannot initiate new PBS-subsidised Ozempic prescriptions for T2D during this window. (Source: pbs.gov.au medicine item 12075M and 12080T)

Eli Lilly's orforglipron (Foundayo) received FDA approval on April 1, 2026, becoming the first small-molecule oral GLP-1 receptor agonist for weight management — taken once daily with no food or water restrictions. Lilly confirmed it has submitted orforglipron to regulators in 40+ countries, including Australia. The FDA approval was the fastest ever for a new molecular entity (approved 50 days after filing, 294 days ahead of schedule, via the Commissioner's National Priority Voucher program). Phase 3 ATTAIN-1 data showed 12.4% mean weight loss at 72 weeks. US self-pay starts at ~USD$149/month for the lowest dose (~A$210). (Sources: Lilly investor release 1 Apr 2026; Pharmacy Daily 9 Apr 2026; Aesthetic Medical Practitioner 9 Apr 2026)

TGA enforcement, shortage declarations, telehealth access, and grey-market alerts.

The TGA issued a formal safety warning on April 14, 2026, flagging an "explosion of illegal peptide use" involving unapproved products including BPC-157, GHK-Cu, TB-500, retatrutide, and CJC-1295. The ABC reported hospitalisation cases including severe allergic reactions, inflammation, palpitations, pain, insomnia, blurred vision, and musculoskeletal injuries. The Australian Medical Association's public health committee called for more aggressive regulatory measures. The warning explicitly covers healthcare practitioners who compound, prescribe, or supply these products. "Black market GLP-1s flood Australia" was the contemporaneous framing in MedNews (March 2026). (Sources: TGA newsGP 14 Apr 2026; ABC News 14 Apr 2026; RACGP newsGP 14 Apr 2026)

The TGA accepted a court-enforceable 3-year undertaking from Your Solution Compounding Pharmacy Pty Ltd, relating to the unlawful advertising of compounded semaglutide and tirzepatide between November 2023 and June 2024. The pharmacy acknowledged its website likely unlawfully promoted prescription medicines. Under amendments effective October 1, 2024, compounded GLP-1 RA products can no longer be compounded by pharmacists or supplied to patients. The TGA confirmed it will continue enforcement action. (Source: TGA media release, tga.gov.au; Diabetes Australia 20 Apr 2026)

Industry analysts have raised concern that the rapid scaling of Indian generic semaglutide production — with 15+ manufacturers producing at prices 90% below branded — will result in leakage into markets where semaglutide remains patent-protected, including Australia. Ben van der Schaaf of Arthur D. Little stated: "If India is starting to manufacture GLP-1s at a large scale, that will not all stay in India, whatever companies try, countries try to prevent it from coming in. It's big business." TGA previously warned of counterfeit Ozempic pens imported into Australia. The Personal Importation Scheme provides a known pathway for individual consumers. (Sources: CNBC 23 Mar 2026; Chemistry World Apr 2026; TGA safety collection) *[speculative for Australia-specific volume]*

Semaglutide and tirzepatide patent expiries, generic applications, biosimilar pipelines, and Australian timeline implications.

On March 20, 2026, Novo Nordisk's core semaglutide patent (IN262697B) expired in India. Within 48 hours, over 15 generic versions had launched from Sun Pharma (Noveltreat, Sematrinity), Dr Reddy's (Obeda), Zydus (Semaglyn, Mashema, Alterme), Lupin (Semanext, Livarise via Zydus), Alkem (Semasize, Obesema), Glenmark (GLIPIQ), Natco (Semanat, Semafull), Torrent (Sembolic, Semalix), Eris (SUNDAE), and Mankind (Samakind) — totalling 20+ brand names. Branded Ozempic costs ₹8,800–11,175/month in India; cheapest generic (Natco) launched at ₹1,290/month. Sun Pharma launched at ₹750–2,000/month. Nomura Research projects the Indian semaglutide market to grow from ₹1,600 crore to ₹12,000 crore over five years. India's Delhi High Court denied Novo Nordisk's request for an injunction to delay generic entry. China's patent also expired in March 2026. (Sources: Business Standard 21 Mar 2026; Asia IP 20 Mar 2026; CNBC 23 Mar 2026; Chemistry World Apr 2026; India Briefing 2026)

Dr Reddy's CEO Erez Israeli stated the company plans to launch generic semaglutide in 87 countries including Canada, Turkey, and Brazil — markets where the patent has expired or lapsed. Canada's semaglutide patent lapsed after Novo Nordisk missed a maintenance fee payment (confirmed June 2025), yet no generic has appeared in Canada as of April 2026 due to regulatory timelines. Biocon plans to export from a new ₹100-crore injectables facility in Bengaluru, aiming for Brazil and Canada launches in 2027. At current Indian generic prices (~USD$8–40/month), the landed cost in patent-free markets is commercially disruptive. (Sources: CNBC 23 Mar 2026; CNN 7 Feb 2026; Chemistry World Apr 2026)

Novo Nordisk announced on February 24, 2026 it will cut the US monthly list price of Wegovy and Ozempic from ~$1,350 to $675 from January 2027 — a 50% reduction — to compete with Eli Lilly and address Trump administration pressure. Novo also warned in February that sales could decline 5–13% in 2026 due to generic competition in patent-expired markets (India, China, Brazil, Canada). Novo had already launched Wegovy injections for cash payers at USD$349/month and the new pill at USD$149/month. (Sources: CNBC 24 Feb 2026; CNN 24 Feb 2026; Guardian 5 Jan 2026)

Phase 2/3 readouts, new indications, real-world evidence, and prescribing data.

A peer-reviewed preprint published on MedRxiv (March 19, 2026) estimated that 39.7% of Australian adults — 7.8 million individuals (95% CI: 7.6–8.1 million) — are eligible for GLP-1RA use under TGA-approved indications for chronic weight management. Of those, 338,900 also meet the criteria for secondary CVD prevention (the current narrow PBS proposal criteria). A separate October 2025 study estimated ~480,000–500,000 Australians use GLP-1 RAs monthly, with 180,000–240,000 buying privately for weight loss. This creates a utilisation gap of roughly 7.3 million eligible but untreated Australians. (Sources: MedRxiv 10.64898/2026.03.17.26348659, March 2026; companion prescribing study October 2025)

Novo Nordisk launched oral Wegovy (semaglutide 25mg tablet) in the US on January 5, 2026, following FDA approval December 22, 2025 — the first oral GLP-1 approved for weight management. The once-daily tablet uses salcaprozate sodium (SNAC) technology to improve peptide absorption. Phase 3 OASIS 4 trial showed 13.6% mean weight loss at 64 weeks (79.2% achieved ≥5% weight loss vs 31.1% placebo). US self-pay price: USD$149/month (≈A$210). UK MHRA is reviewing; TGA status in Australia not yet confirmed. An Australian GP guide (March 2026) suggested oral Wegovy "may be available in Australia by late 2026." (Sources: Guardian 5 Jan 2026; AJMC 2 Apr 2026; Crown St Medical Centre Mar 2026)

The FDA approved Eli Lilly's orforglipron (Foundayo) on April 1, 2026 — the first small-molecule (non-peptide) oral GLP-1 receptor agonist for weight management. Unlike oral semaglutide, Foundayo has no food or timing restrictions — taken any time of day. ATTAIN-1 trial: 12.4% mean weight loss at 72 weeks. ATTAIN-1 enrolled participants across the U.S., Brazil, China, India, Japan, South Korea, Puerto Rico, Slovakia, Spain, and Taiwan. US self-pay price: USD$149/month (≈A$210). Lilly has submitted in 40+ countries including Australia. FDA approval was the fastest NME approval since 2002 (50 days post-filing via National Priority Voucher program). (Sources: Lilly investor release 1 Apr 2026; Pharmacy Daily 9 Apr 2026; Medical News Today 8 Apr 2026)

SURMOUNT-5, the first head-to-head randomised trial between tirzepatide and semaglutide, published in NEJM (May 2025), showed tirzepatide achieved 20.2% mean weight loss vs 13.7% for semaglutide at 72 weeks. A Frontiers in Medicine narrative review (published April 22, 2026) synthesised SURMOUNT-5 alongside cardiovascular and glycaemic outcomes from multiple Phase 3 programs. An April 2026 Nature Genetics study (n=27,885) identified GLP1R and GIPR variants predicting response and side-effect risk — individuals with risk alleles at both loci had 14.8-fold higher odds of tirzepatide-related vomiting. (Sources: NEJM May 2025; Frontiers Med 22 Apr 2026; Nature Genetics Apr 2026)

Australian pharmacy chain moves, scope-of-practice changes, retail category data, and wholesaler signals.

Sigma Healthcare (ASX: SIG), which merged with Chemist Warehouse, reported H1 FY26 results on February 26, 2026. Australian Chemist Warehouse (CW) branded store sales grew 17.2% to $5.1 billion, with like-for-like sales up 15.0%. Group revenue reached $5.5 billion (+14.9%). Normalised net profit rose 19.2% to $392.0 million. CEO Vikesh Ramsunder explicitly attributed "structural uplift" from GLP-1 medicines as a key driver and stated that demand would "actually increase the market size over time as it becomes cheaper" — specifically referencing anticipated oral GLP-1 forms. The AFR separately noted "Ozempic makes Chemist Warehouse profits even fatter." 550 CW-branded Australian stores operating as of H1 FY26. (Sources: Sigma ASX announcement 26 Feb 2026; AFR 26 Feb 2026; The Nightly 26 Feb 2026)

Multiple parties including Chemist Warehouse (via Sigma), AS Watson (Watsons/Superdrug), and Bain Capital were reported as interested in purchasing Priceline stores from the Infinity Pharmacy Group. The Pharmacy Guild separately flagged ACCC concerns about Chemist Warehouse's potential acquisition of Priceline locations. This consolidation activity directly affects how GLP-1 dispensing volume concentrates in Australian pharmacy retail. (Sources: AFR 1 Feb 2026; 22 Feb 2026)

Minister Butler's January 12 statement confirmed 400,000+ Australians pay private prices for GLP-1 medicines — up to $5,000/year. Wegovy private price: ~$400–460/month. Mounjaro (tirzepatide): $285–645/month. Ozempic (for weight use, not T2D): ~$130–200/pen privately. PBS-subsidised Ozempic for T2D: $25/script. The companion prescribing study estimated 180,000–240,000 Australians purchasing privately each month for weight loss alone. (Sources: ABC News 12 Jan 2026; fitnessnetwork.com.au; clinicalevidence.net.au)

Consumer awareness, supplement category shifts, food brand pivots, and GLP-1 cultural signals.

SBS News reported in 2026 that GLP-1 drug adoption is "already reducing food and beverage consumption by one to two per cent" in Australia, driven primarily by the US and with Australia beginning to follow. Multinational companies including Nestlé, Danone, and Coca-Cola are launching high-protein, high-fibre, low-sugar products targeting GLP-1 users. Flinders University research suggests GLP-1 drugs could reverse a three-decade trend of energy-dense food consumption. Australian restaurants are not yet offering "Ozempic menus" unlike the US (as of early 2026). A medRxiv study noted GLP-1 users can reduce overall food intake by 20%, but may fall short on protein, fibre, and calcium. (Sources: SBS News 2026; Nutrition Insight Jan 2026; Ingredion 2026; Glanbia Nutritionals MegaTrends 2026)

Global research confirms 39% of GLP-1 users discontinue within 3 months and 50% within 12 months, driving significant weight regain — creating a major supplement maintenance opportunity. GLP-1 use reduces total food intake by ~20%, but can leave patients short on protein (target: 1.2–1.6g/kg bodyweight), fibre, calcium, B12, and magnesium. Research (Brighton Spinal, 2026) notes 20–40% of weight lost on GLP-1s may come from lean tissue, making protein supplementation clinically validated. Nutraceuticals World (2026) flagged that traditional fat-burning/appetite-suppression supplements are losing relevance, while muscle-preservation, fibre, and nutrient-density supplements are gaining. Australian GP practices (Crown St Medical Centre, March 2026) are beginning to formally recommend protein-rich dietary patterns alongside GLP-1 prescriptions. *[Australian-specific supplement sales data not yet available — emerging signal]* (Sources: Ingredion 2026; NutraceuticalsWorld 2026; Brighton Spinal 2026; Glanbia MegaTrends 2026)

Glanbia Nutritionals MegaTrends 2026 report cited weight management as the No.1 physical health concern globally (38% of consumers), with 36% ranking mental/emotional wellness as their top health goal. GLP-1 medications have "entered the mainstream" per Glanbia, creating new consumer expectations around nutrient density, satiety, hydration, and everyday food choices. Nutraceuticals World noted half of supplement consumers "do not understand the evidence" behind traditional weight management products — creating a re-education opportunity for GLP-1-aligned supplement brands. *[speculative for AU-specific consumer sentiment without local survey data]* (Sources: Glanbia MegaTrends 2026; Nutraceuticals World 2026)

The PBS listing of Wegovy is the most consequential event in Australian weight management history — prepare for it now, not after it happens. Health Minister Butler's commitment and the PBAC recommendation signal this is a matter of when, not if. The narrow initial criteria (BMI ≥35 + CVD) targets approximately 338,900 patients, but the precedent it sets — a government-subsidised GLP-1 for weight management — is irreversible. Novo Nordisk's global pricing pressure (50% US list price cut announced February 2026) and the Indian generic market collapse (90% price drop on Day 1 in India) will compress Novo's negotiating leverage in Australia. Pharma commercial teams, pharmacy buyers, and health investors should model scenarios assuming a PBS listing in late 2026 or Q1 2027, with initial annual government cost in the $300–500 million range based on PBAC guidance.

Eli Lilly's PBS standoff is the defining risk signal for GLP-1 access equity in Australia. Four failed PBAC submissions for Mounjaro — a drug with demonstrably superior weight loss outcomes (20.2% vs 13.7% in SURMOUNT-5) — mean that a better product remains inaccessible to most Australians on cost grounds. Lilly's April 2026 withdrawal of the PBS application is not a permanent exit — it is a negotiating move. The outcome of this standoff will determine whether tirzepatide enters the PBS in 2027 or 2028, and will set the template for how Australia prices next-generation dual-agonist GLP-1s. For pharmacy buyers: do not write off PBS-subsidised Mounjaro — continue stocking at private prescription levels and plan for volume upside if Lilly and the government reach terms.

The Indian generic launch of March 20, 2026 is a 5–10 year signal, not an immediate Australian event — but act on it now. Australia's semaglutide patents are protected until the 2030s, so generic semaglutide cannot enter the Australian market legally in the near term. However, India's mass production of semaglutide at ₹750–4,200/month is setting the global pricing floor that will inform every PBAC cost-effectiveness submission from this point forward. Parallel import risk via the Personal Importation Scheme is real: TGA has previously detected counterfeit Ozempic imports, and the volume of Indian production creates grey market pressure. Border surveillance and supply chain integrity will become an active PBAC and TGA concern over the next 18 months.

Chemist Warehouse's 17.2% GLP-1-driven sales growth is a structural outcome, not a one-off windfall — the oral GLP-1 wave will amplify it further. Sigma's H1 FY26 results confirm that GLP-1 medicines have already structurally elevated pharmacy revenue. CEO Ramsunder's explicit reference to oral GLP-1 forms as the next demand catalyst signals where management attention is focused. With oral semaglutide (Wegovy pill, US-launched January 2026) and orforglipron (Foundayo, FDA-approved April 1, 2026) both submitted to TGA — and potentially available in Australia by late 2026 — the dispensing volume growth is not yet priced into CW's full-year trajectory. For competing pharmacy models, the window to build GLP-1 category leadership is rapidly narrowing.

The 7.3 million gap between TGA-eligible Australians (7.8M) and current users (~500K) is the defining market opportunity of the next decade — and supplement brands should position for it now. Even at the narrow PBS criteria, the pathway to broadened access is inevitable: initial PBS listings routinely expand criteria as real-world cost data matures. As access expands, so does the need for companion nutrition support — protein supplementation for muscle preservation (20–40% of GLP-1 weight loss comes from lean tissue), fibre for gut function, B12 and magnesium for long-term adherence, and maintenance products for the 50% who discontinue within 12 months. Chemist Warehouse, Priceline, and TerryWhite chains that develop clinical GLP-1 companion ranges — in partnership with GPs and endocrinologists — will capture the largest share of this emerging category.